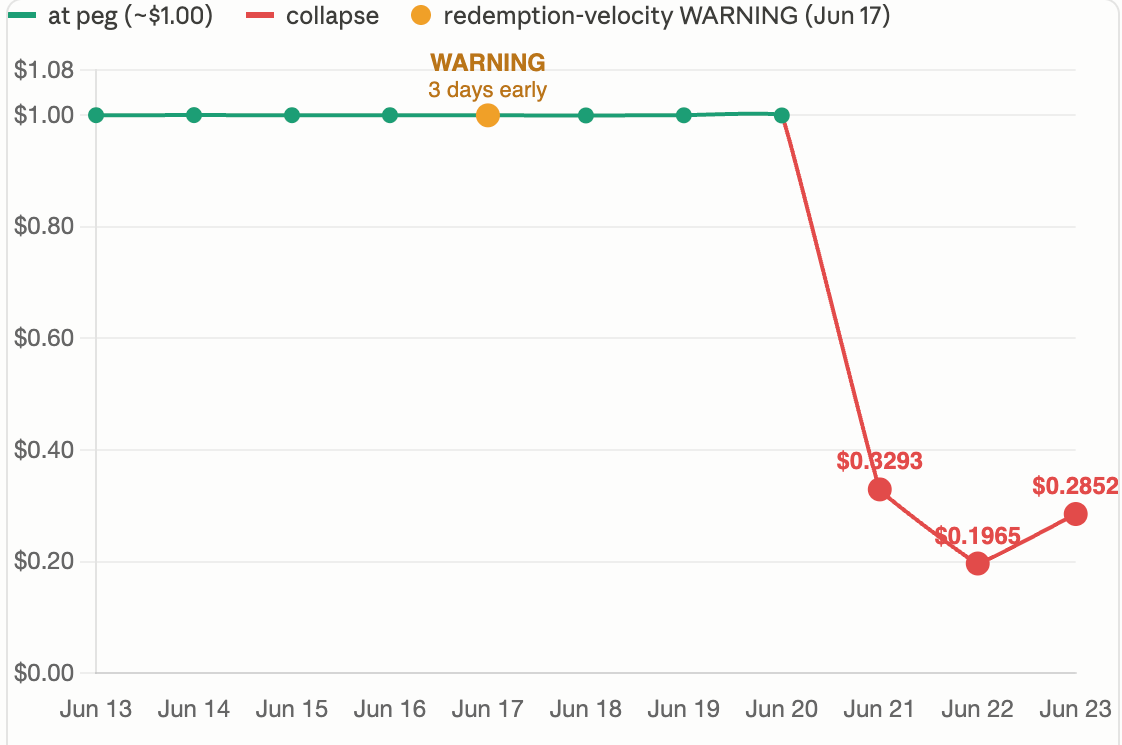

On June 20, 2026, Main Street USD (msUSD) lost its dollar peg and fell roughly 80% in a day, from $1.00 toward $0.20. The public trigger was abrupt: Accountable, the third-party provider that verified msUSD's reserves, terminated its agreement with the protocol, and confidence in the backing evaporated within hours. But by the time the price moved, the informed money was already gone. In the five days before the collapse, two wallets had quietly redeemed roughly $8 million of msUSD, close to 11% of the entire supply, at par. They took their dollars out at $1.00. Everyone still holding when the peg broke is now marked near $0.20.

This is the kind of depeg that price monitoring is structurally blind to. No key was compromised, no oracle broke, nothing was minted out of thin air, no contract was exploited. msUSD redeemed one-for-one for its backing the entire time, exactly as designed, and the peg sat at $0.999 on a dead-flat line through June 20. Anyone watching the price, or any system scoring only price deviation, velocity, and volume, would have seen a perfectly healthy dollar token right up until the cliff.

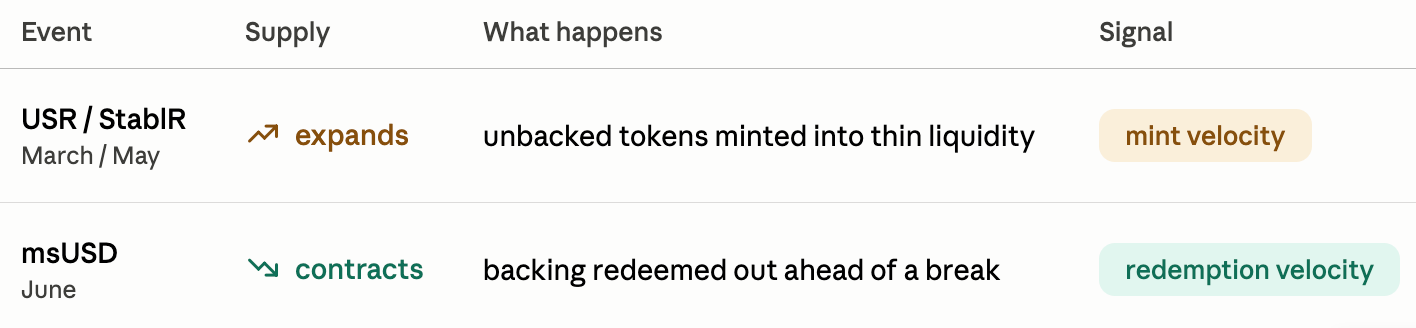

The warning was there days earlier, in a different place entirely: not in the price, but in the supply. Specifically, in the rate at which supply was being redeemed and how few wallets were doing it. It is the mirror image of the USR and StablR attacks we documented earlier. Those were supply expansions, unbacked tokens minted into the market, and our mint-velocity monitoring catches that growth before the price reacts. msUSD was the opposite, a supply contraction: a concentrated redemption run draining the backing ahead of a break. The same principle runs in reverse, and it is just as legible on-chain.

What The Price Showed: Nothing, Until It Was Over

Main Street USD is a yield-bearing dollar stablecoin on Ethereum, with a staked counterpart

(Staked msUSD / msY) that accrues yield from options-arbitrage strategies. Supply at the time

of the event was approximately 74.2 million msUSD. Redemption was open the entire period: msUSD holders could burn their tokens for the underlying dollar backing at par. Here is the daily price, the only thing a price-first monitor would have on this token:

For eight days the daily mark sits inside a 7-basis-point band around a dollar. There is no acceleration, no widening deviation, no velocity spike, no volume anomaly that a price model would score. The peg does not erode; it holds perfectly on the daily mark and then falls off a cliff over June 20-21. Every price-derived risk signal reads "ok" through the June 20 open because, on price, msUSD was fine until then. The information that mattered was not in the price. It was in the supply.

The Public Trigger: A Verification Feed, Cut

The proximate cause of the cliff was not on-chain. On June 20, Accountable, the third-party provider that attested to msUSD's reserves, terminated its agreement with MainStreet, stating the protocol could not meet its verification standards. With the feed switched off, nothing was publicly verifying the backing, and the market repriced the token toward zero within hours. MainStreet disputed the framing, maintaining that msUSD remained fully backed and that the problem was the verification feed rather than the assets, and said it had deployed more than $8 million in USDC to support liquidity.

That liquidity figure needs to be held apart from the others in this story, because three roughly-$8-million numbers collide here and conflating them would be a real error. The $8 million of USDC MainStreet deployed is protocol-side liquidity support. The day's trading volume was separately reported near $8.25 million. And the ~$8 million this post is about is something else entirely: msUSD that two wallets redeemed at par in the days before the feed was cut. Same magnitude, three different stories.

What Was Happening Underneath: An $8M Redemption Run

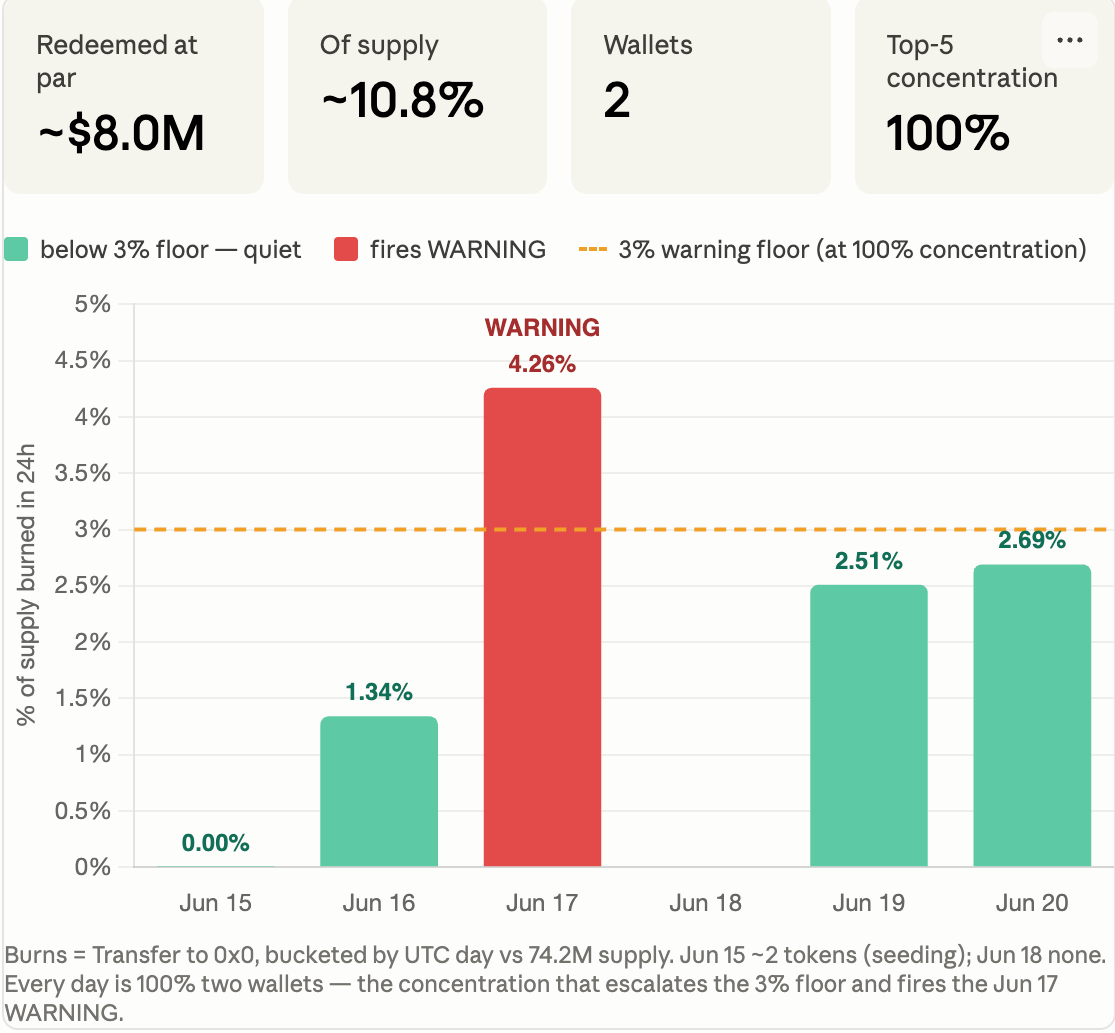

A redemption of msUSD is a burn: the token is sent to the zero address and the backing is released to the redeemer. Burns are on-chain Transfer events to 0x000...000, and they are fully legible in real time, the same way mints are. Summing the burns by day, against a ~74.2M supply, gives the picture the price was hiding:

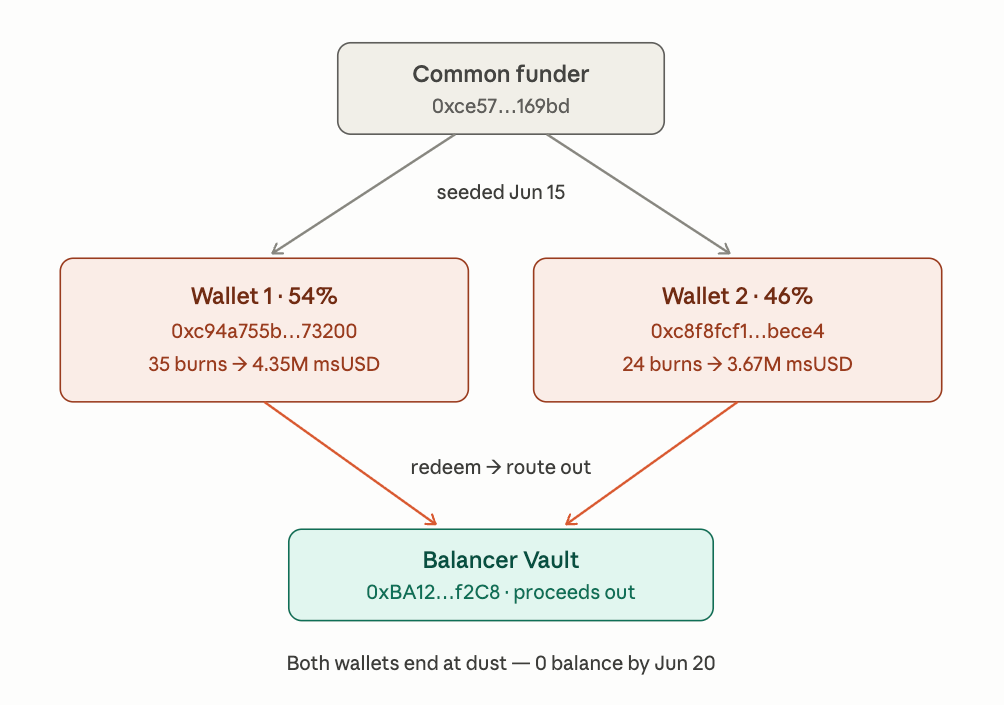

Roughly $8 million of msUSD, redeemed at par, by two addresses, over five days, while the price never left peg. The concentration is the tell. This was not a market of holders broadly heading for the exit, which is ordinary and not by itself alarming. Every burn in the window traces to just two wallets:

0xc94a755bce57b88177636cf03035010461e73200 ~54% of redeemed volume

0xc8f8fcf1a7780935b281a00e4e997284c06bece4 ~46% of redeemed volume

Both addresses are smart-contract wallets, activated on June 15 by one operator EOA (0xce57c04483ea2ff43bb4a8412cd9350cf2c169bd), which sent only small USDC gas seeds (~$51 and ~$10), not the millions that followed. Over the next five days the two wallets acquired their msUSD on-chain, redeemed it at $1.00, and routed the dollar proceeds back out through Balancer. By June 20, when Accountable cut the feed and the price broke, both held zero msUSD and only dust. Two contract wallets, one operator, coordinated timing, and full exits at par before the public collapse: on the on-chain evidence this looks like informed redemption ahead of a break, the exact shape a price model cannot represent and a supply model surfaces immediately.

The Signal: Redemption Velocity, Gated By Concentration

Our stablecoin monitor already scores on-chain supply expansion, the mint-velocity signal that flagged the USR and StablR minting attacks. We also have its mirror: a redemption-velocity signal that scores supply contraction. We alert on anomalous redemption/burns that hit a threshold percentage of asset supply, and alert for burn volume coming from the concentration of burner wallets. This is next-level risk intelligence that leads to actionable, predictive monitoring, rather than relying on price feeds after the fact.

Velocity alone is not the alarm. Stablecoins are redeemed every day; large, broad redemptions are normal market behavior and should not page anyone. The differentiator, the thing that separates a quiet bank run from ordinary turnover, is concentration. A few wallets draining a large share of supply is the run/insider pattern that precedes a break. So the signal is velocity gated by concentration: a redemption burst is only escalated when the top-concentration burners account for at least a certain percentage of the volume, and the alert tier steps up when that share exceeds another higher threshold. (Talk to us for the details 😉)

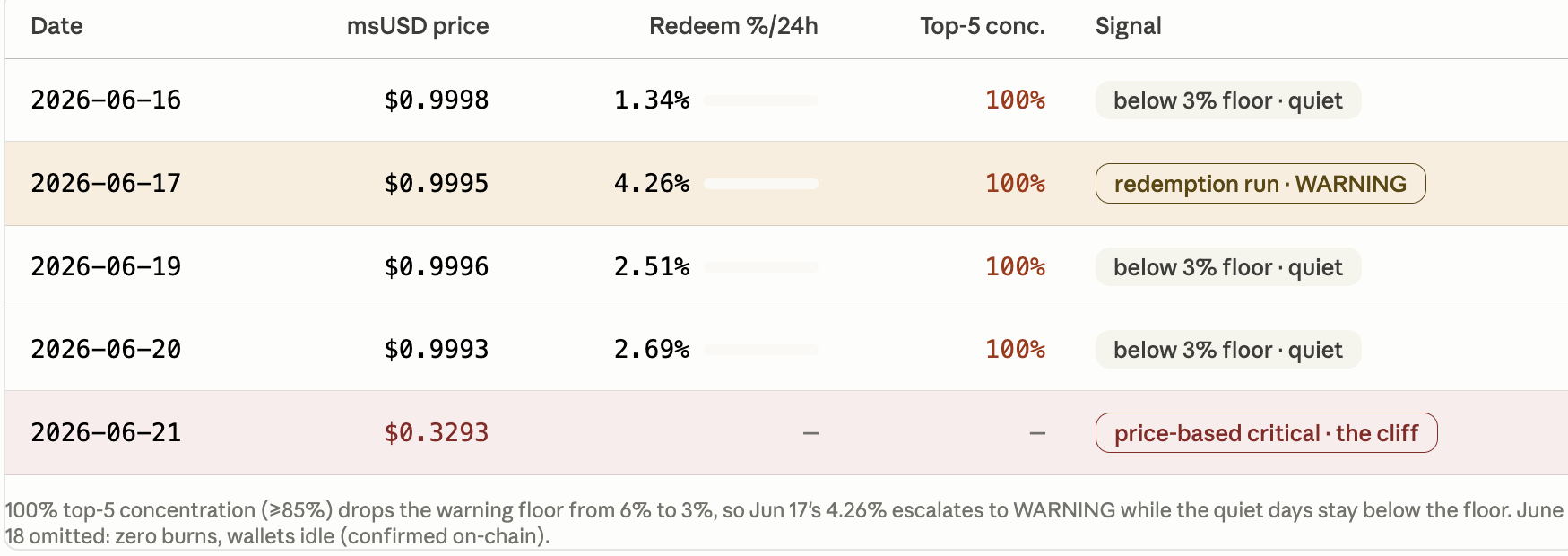

Replayed against the on-chain msUSD record, here is what the signal emits, day by day, with the price it had been carrying at the time:

On June 17, three days before the price broke, 4.26% of msUSD supply was redeemed in 24 hours and 100% of it is two wallets. On velocity alone, 4.26% is only a watch; but with the entire drain in two wallets, concentration is past the 85% escalation line, which steps the alert up one tier to a WARNING (in the Webacy alert system) -- while msUSD is trading at $0.9995 and every price-derived score on the token still reads "ok." That is the entire thesis of structural monitoring in one row: the verdict that mattered was available days before the price delivered the same verdict for free.

Supply Is A Two-Directional Signal

USR (March), StablR (May), and msUSD (June) looked like different kinds of failure: USR and StablR were minting attacks, msUSD a redemption run. But they all end the same way, a dollar token knocked off its peg, and underneath they're the same measurement. A stablecoin's backing is its supply, and the moments that matter are the ones where that supply moves fast and narrowly, in either direction:

Either way, it's the same primitive: a Transfer at the zero address, minted from it or burned to it, visible the moment it lands in a block, well before the price has had a chance to react. And either way, a price-only monitor sails right past it: in all three cases the token was still sitting at or near peg while the supply signal was already screaming. So we now score both directions. On the expansion side it's mint velocity (rolling and single-block); on the contraction side it's redemption velocity gated by wallet concentration. Both run alongside a reserve-attestation-freshness check, and all of it feeds the vault and collateral risk layer described below.

The Contagion: Vaults Denominated In msUSD

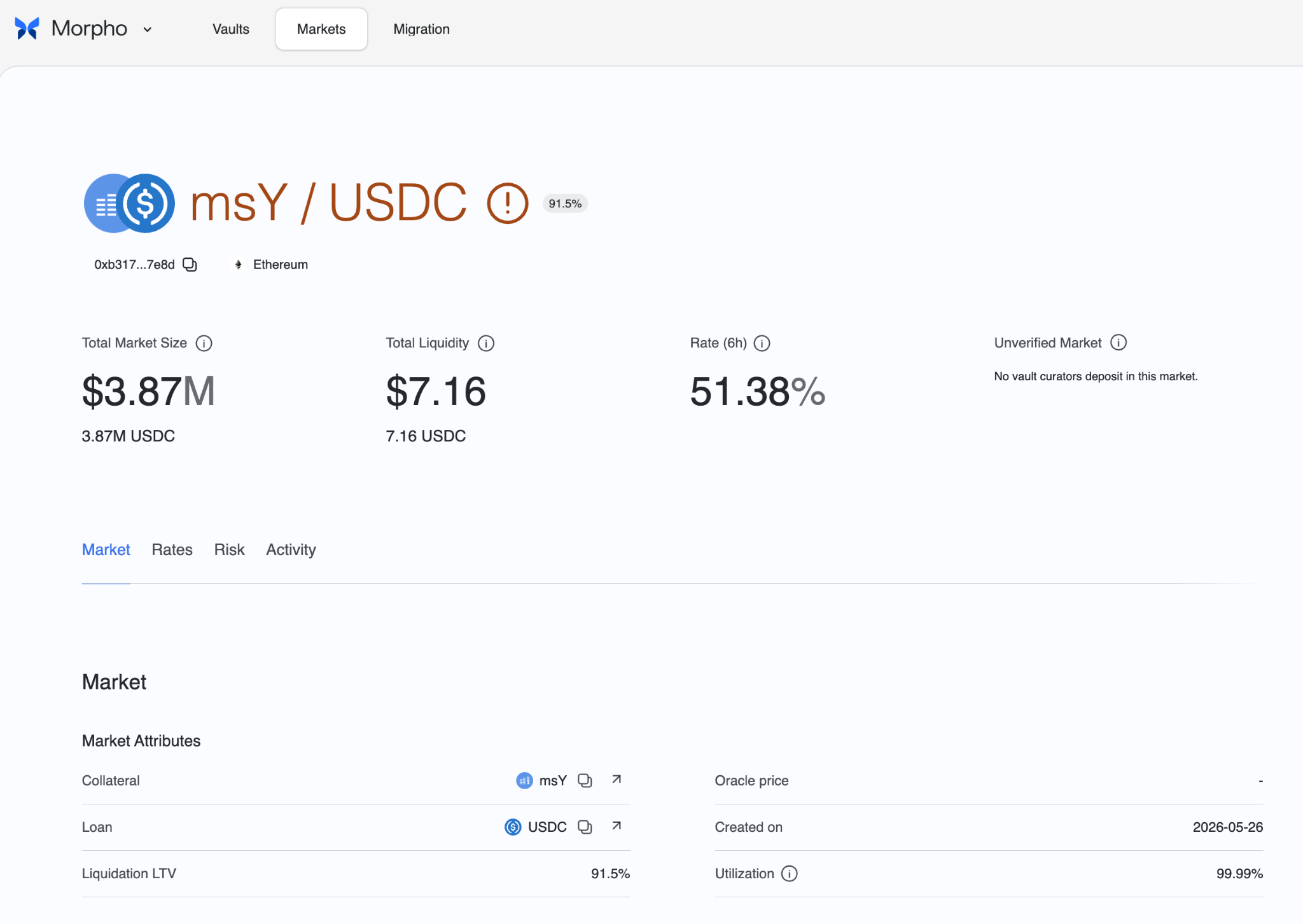

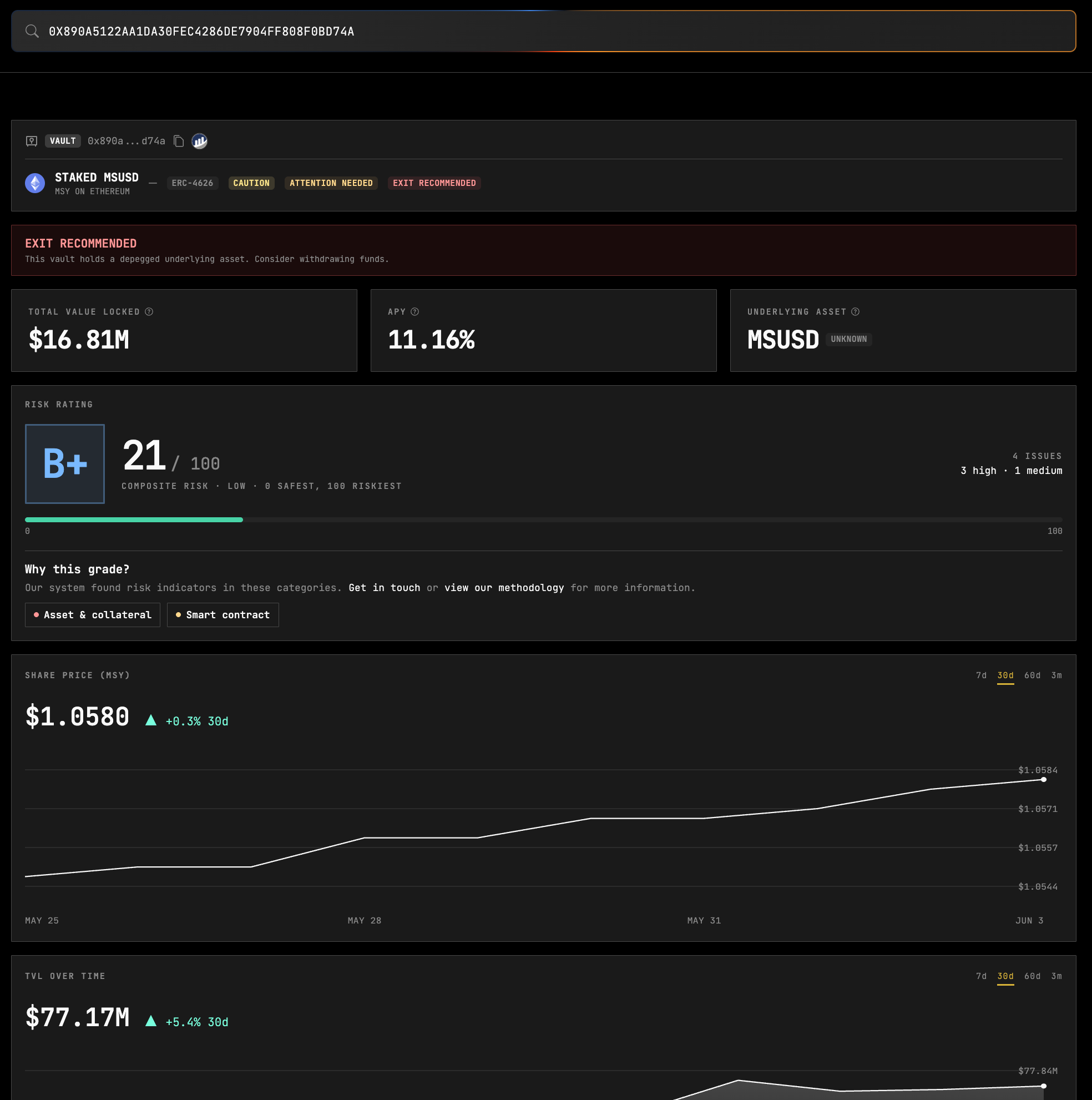

A depegged stablecoin is only the first-order loss. The second-order loss is every vault, lending market, and LP that holds it as collateral or denomination, and those positions do not reprice themselves the instant the underlying breaks. The clearest case is Staked msUSD (msY), the staking vault for msUSD: a standard ERC-4626 vault holding about 67.6 million msUSD*. In msUSD terms its share price held and even climbed, to roughly $1.06 per share, and the dashboard still shows an 11.16% APY*, so a vault view reading only share price and yield would call it healthy. In dollar terms it is not. The vault is worth about $16.8 million today*, down from roughly $67.6 million at peg, a ~75-80% loss that tracks the underlying as msUSD trades in the low $0.20s, with redemptions still open.

*note - all values are at the moment of writing, values may have changed at the time of reading

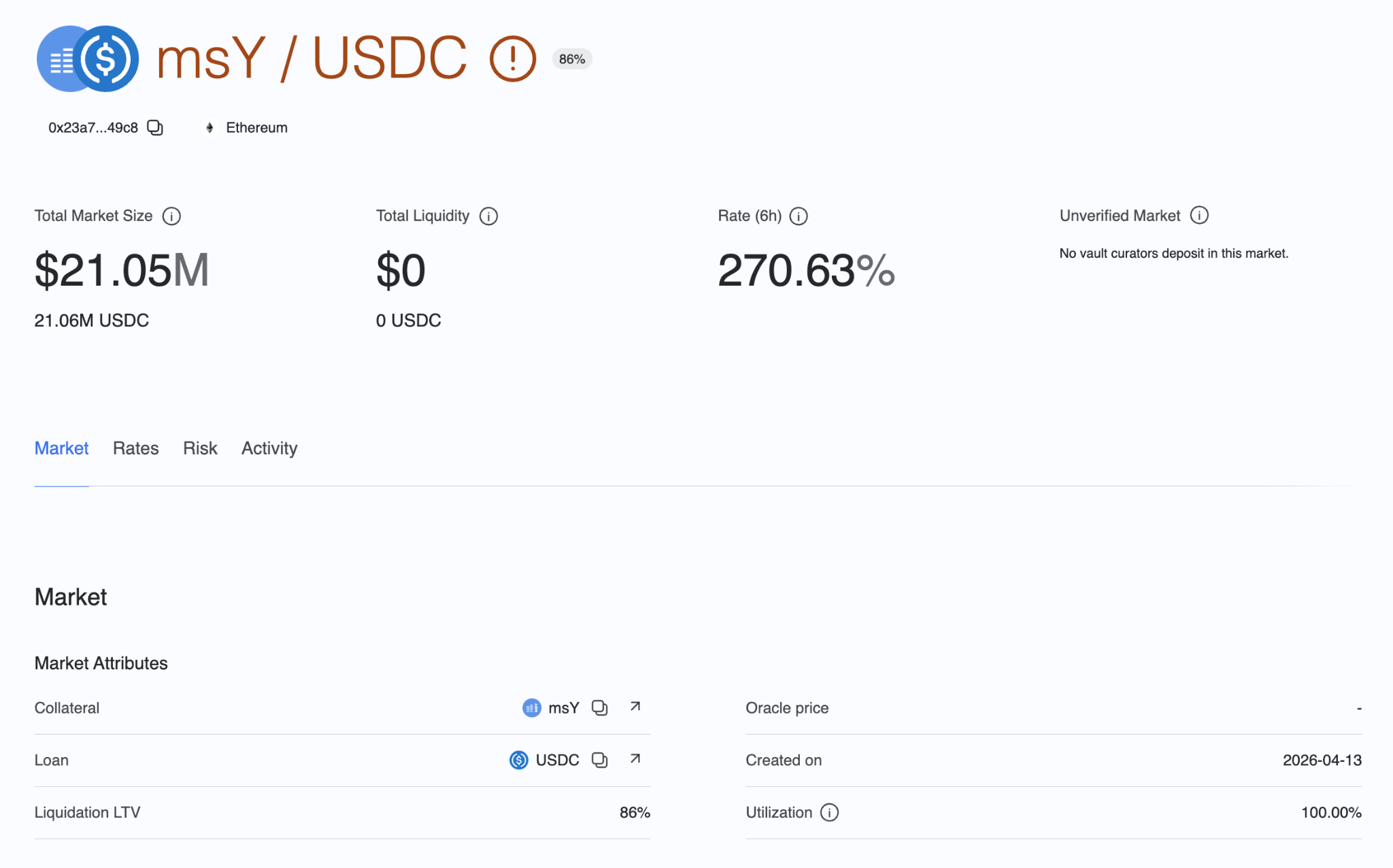

The damage propagated one layer up, into the lending markets that take msY as collateral. The Morpho API shows two live msY/USDC markets on Ethereum, both pinned at 100% utilization with essentially no withdrawable liquidity: about $21.0M of USDC supplied against the 86%-LLTV market and another $3.9M against the 92%-LLTV market, roughly $25M borrowed against msY collateral that lenders now cannot pull out. (That ~$25M of downstream lending exposure is a separate figure from the ~$16.8M dollar value of the Staked msUSD vault itself; they are different positions.) Public reporting attributed roughly $18M of that supply to a single Delta-V2 vault, AlphaUSDC. A lending market at 100% utilization is one where lenders cannot withdraw and borrowers cannot be cleanly liquidated, because the collateral is the asset that just collapsed. The depeg becomes a liquidity freeze one layer up.

Our vault risk layer reads the live depeg signal and acts on it. The vault's own mechanics are clean, so its structural composite stays low, a B+ at 21 out of 100, and the share price and APY both still read well. That is exactly the trap. Reading the depegged denomination asset at roughly $0.22, 100% exposure, the system overrides that clean profile with an EXIT RECOMMENDED verdict and asset-and-collateral caution, because a vault whose unit of account has lost three quarters of its value is not a hold no matter how tidy its internals look. A vault told to exit must not be buried under a healthy-looking score.

What It Demands

Nothing about msUSD broke, and that is the uncomfortable part. The contract did exactly what it promised: it let holders redeem at par, and two of them did, at scale, in the days before anyone else learned the peg would not hold. There is no patch for a protocol working as designed. The only defense is to watch the one record that showed the run while it was happening, the supply, and to treat a fast, narrowly held drain of a token's backing as the warning it already is.

And it was legible the whole time. The public coverage of the collapse could only gesture at this after the fact, that "insiders got the memo and took the liquidity." We can name it: two smart-contract wallets operated from one EOA, roughly $8.0 million (~10.8% of supply) redeemed at par in burns to 0x0, with USDC proceeds routed out through Balancer before the price moved a basis point. The press inferred the exit from the wreckage. The chain showed the exit as it cleared, three days earlier.

By the time a dollar token prints $0.33, there is nothing left to catch. The verification dispute is already public, the informed redemptions have already settled, and the holders who were going to get out are gone. Price is the lagging confirmation of a decision that supply recorded first. Mint velocity caught USR and StablR as unbacked tokens were minted into the market; redemption velocity, gated by concentration and wired into vault scoring, catches the mirror case as backing is pulled out from under it. msUSD is the proof that for a dollar token the price was never going to be the first thing to know, and that waiting for it is a choice to be last.

Conclusion

Webacy is the leading risk intelligence company for digital assets. Our asset integrity technology combines onchain signals with cutting-edge safety, financial, and behavioral risk models to enable a monitoring, alerting, and data system for the future of financial markets. In this example our redemption-velocity signal, gated by wallet concentration, triggered a warning alert days before any price action occurred. Webacy's Digital Asset Ratings don't wait for a verification feed to get cut or a price to crater. They read the onchain signal that actually moves first, score it continuously rather than on a snapshot, and trace every alert back to the specific structural condition driving it, so a vault holding a "healthy" 11% APY share price can still be flagged EXIT RECOMMENDED the moment its denomination asset breaks. That's the difference between a rating and a live signal, and it's the only kind of risk intelligence built for a market where the warning shows up onchain days before it shows up in the price.

Sources: crypto.news — MainStreet defends backing · protos.com — Altura winds down vault · KuCoin — msUSD loses peg, -71%/24h · crypto.news — Altura $8.5m redemption rush · startupfortune — vendor termination