Introduction

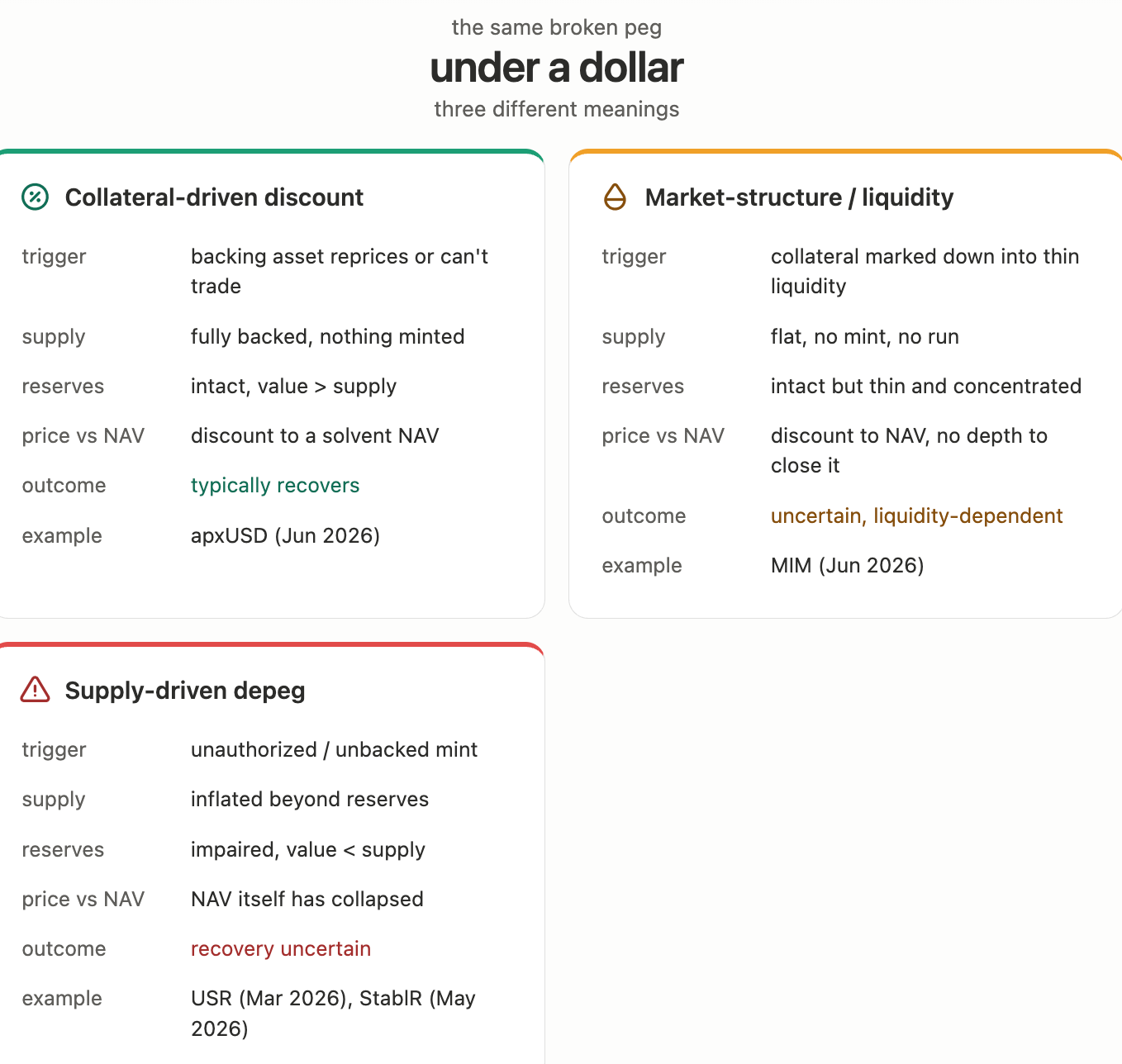

For the last few months this series has mostly tracked stablecoins that broke because of exploits. In March an attacker minted roughly $80M of unbacked USR through a compromised key and the peg broke catastrophically in minutes. In May StablR went the same way, $13.5M through a compromised governance key, the same attack class two months apart. April alone ran to around $635M lost across 28 incidents. The shape was always the same: backing gave way, supply outran reserves, and the price followed. The last two weeks of June broke that pattern. apxUSD and MIM both lost their peg in the same week, and neither was an attack. No compromised key, no unauthorized mint, no missing collateral. A stablecoin can be fully solvent and still trade under a dollar, and that is exactly what happened.

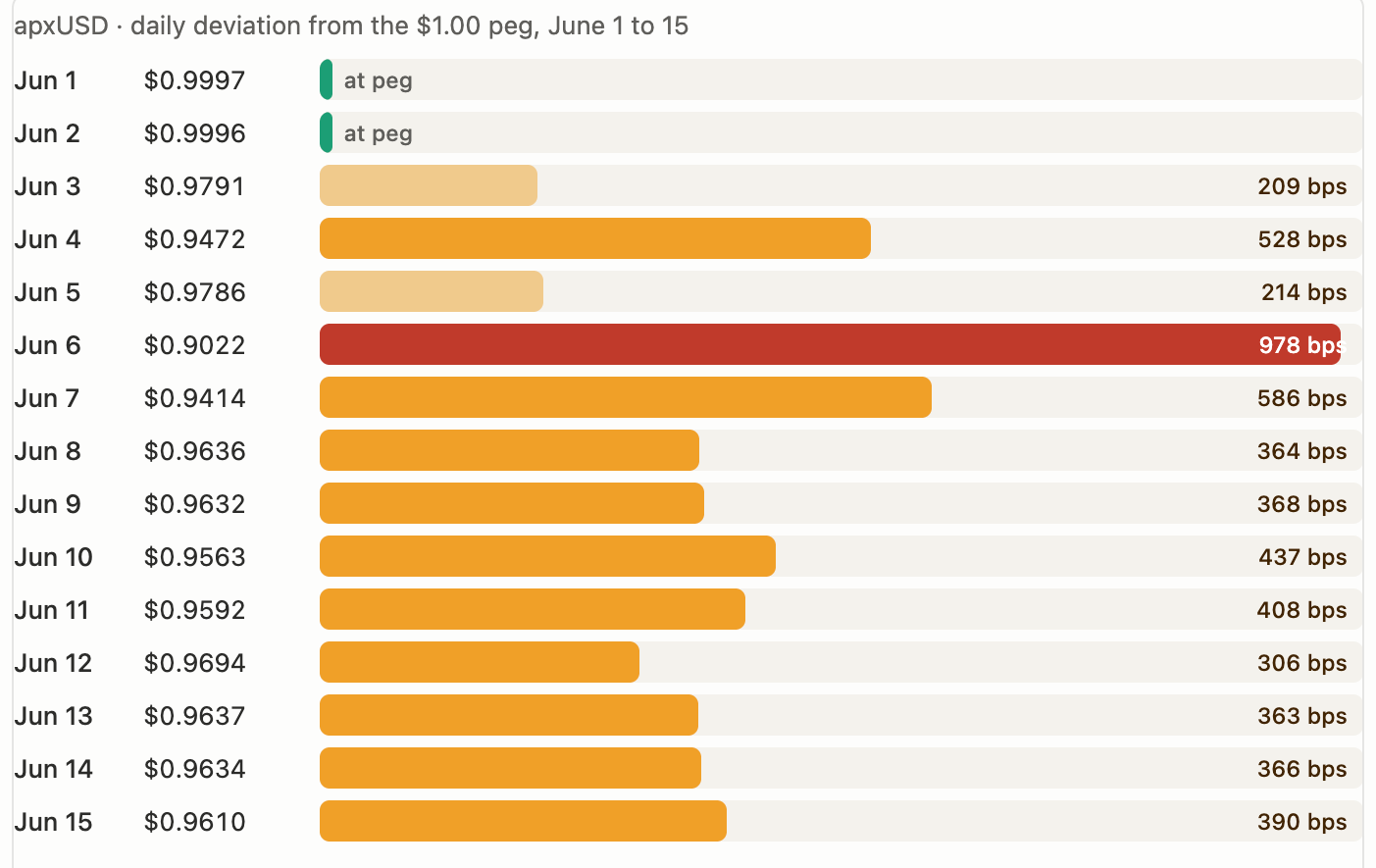

On June 6, apxUSD traded as low as $0.90 with every dollar of its supply still backed. Its collateral simply repriced, and a NAV-following stablecoin did exactly what its design says it will do under stress. It then tracked its collateral back up and now sits near $0.96, still below a dollar only because the collateral itself is still below par.

MIM was the other one, the same week. It is a thin, shrunken crypto-backed stablecoin, down from billions at its peak to roughly $24M, and when its collateral was marked down in the same selloff there was no deep market to absorb the move. It slid more than 11-13% below peg and kept sliding, with no exploit and no redemption run anywhere in the data. On-chain monitors pinned the cause on fragmented, thin liquidity rather than any protocol failure, and unlike apxUSD it has not snapped back, because its recovery depends on liquidity that simply is not there.

A price feed cannot tell any of this apart, not the solvent repricing, not the dead liquidity, and not the exploits that came before. They all print the same number under a dollar. What the feed cannot show is whether the backing is gone, repriced, or just trapped behind closed markets and thin liquidity, and those endings could not be more different. Here is what our systems saw during the apxUSD and MIM depeggings, and why reading a modern depegging means reading the collateral and the order book, not just the distance from a dollar.

APXUSD DEPEGGING EVENT: COLLATERAL REPRICED, NOTHING WAS ATTACKED

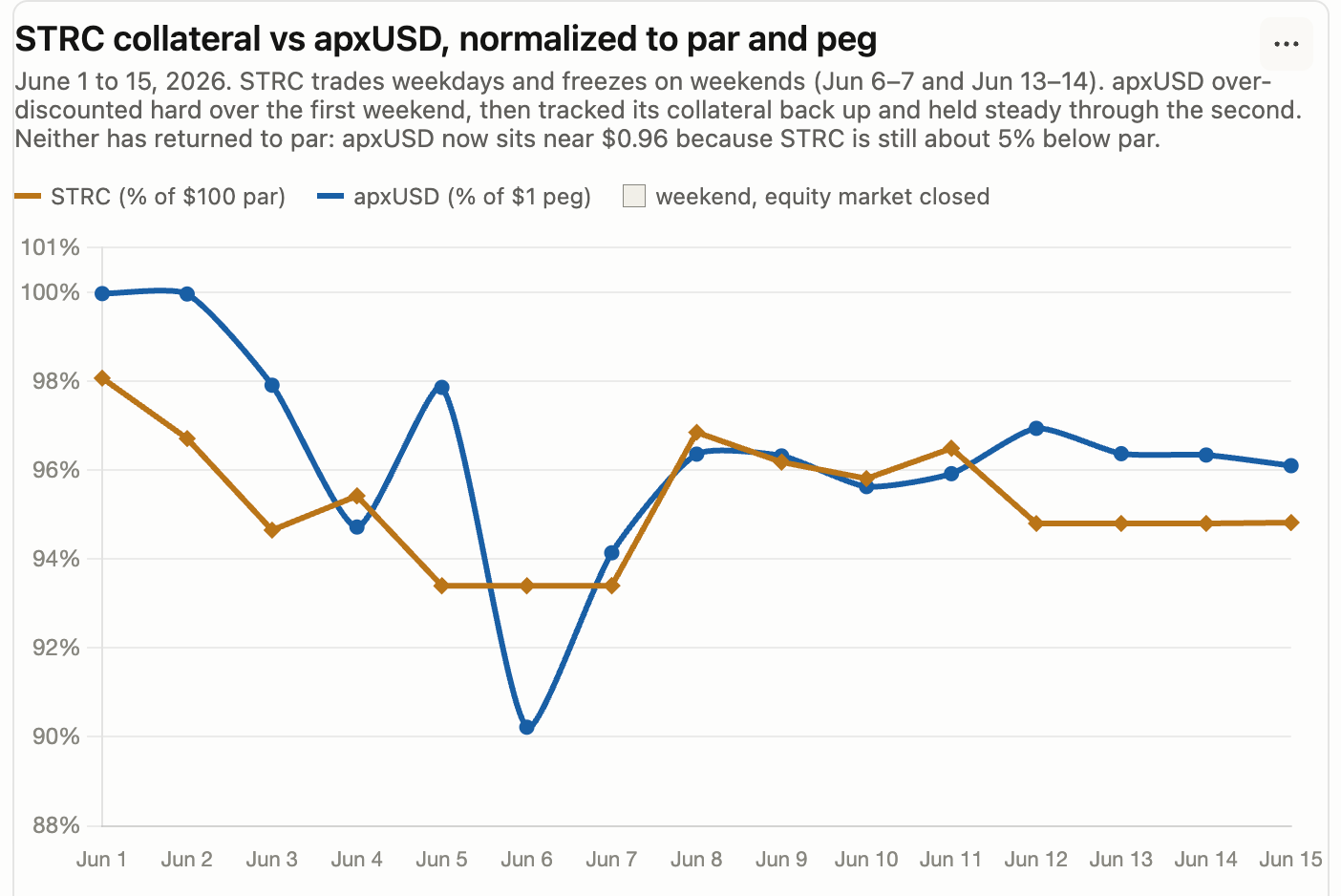

apxUSD is majority-backed by STRC, the variable-rate perpetual preferred share issued by Strategy, with a $100 par value. Apyx holds the shares, collects the dividend, and passes the yield on-chain. The token's value tracks the NAV of that basket, so when the basket moves, the token moves with it.

In the first week of June, Bitcoin fell roughly 30% over a month and almost 20% in a single week, one of the steepest weekly drawdowns in its history. STRC, which is something like 80% retail-held, followed it down from near par to $90.38, its largest drop on record. With reserves concentrated in STRC, apxUSD's NAV compressed, the overcollateralization buffer thinned, and the market price tracked the NAV down to a $0.90 low before settling into the $0.95 to $0.96 range.

Apyx's own post-mortem is blunt about it: the protocol "remained solvent throughout, meaning the value of the reserves continued to exceed the market value of the circulating apxUSD supply, but the market price deviated materially from the NAV." Nothing was stolen. No supply went unbacked. And the worst of the dislocation hit overnight, while U.S. equity markets were closed and STRC literally could not trade.

That makes this a collateral-driven depeg, a different animal from the supply-driven exploits like USR and StablR the market saw earlier this year. The backing did not fail. It repriced, in a market that was closed at the time.

WHAT OUR SYSTEMS SAW

Our DD.xyz stablecoin ratings monitor scores live peg deviation, liquidity, and persistence in real time across multiple chains, here is the daily summary of what apxUSD looked like on Ethereum:

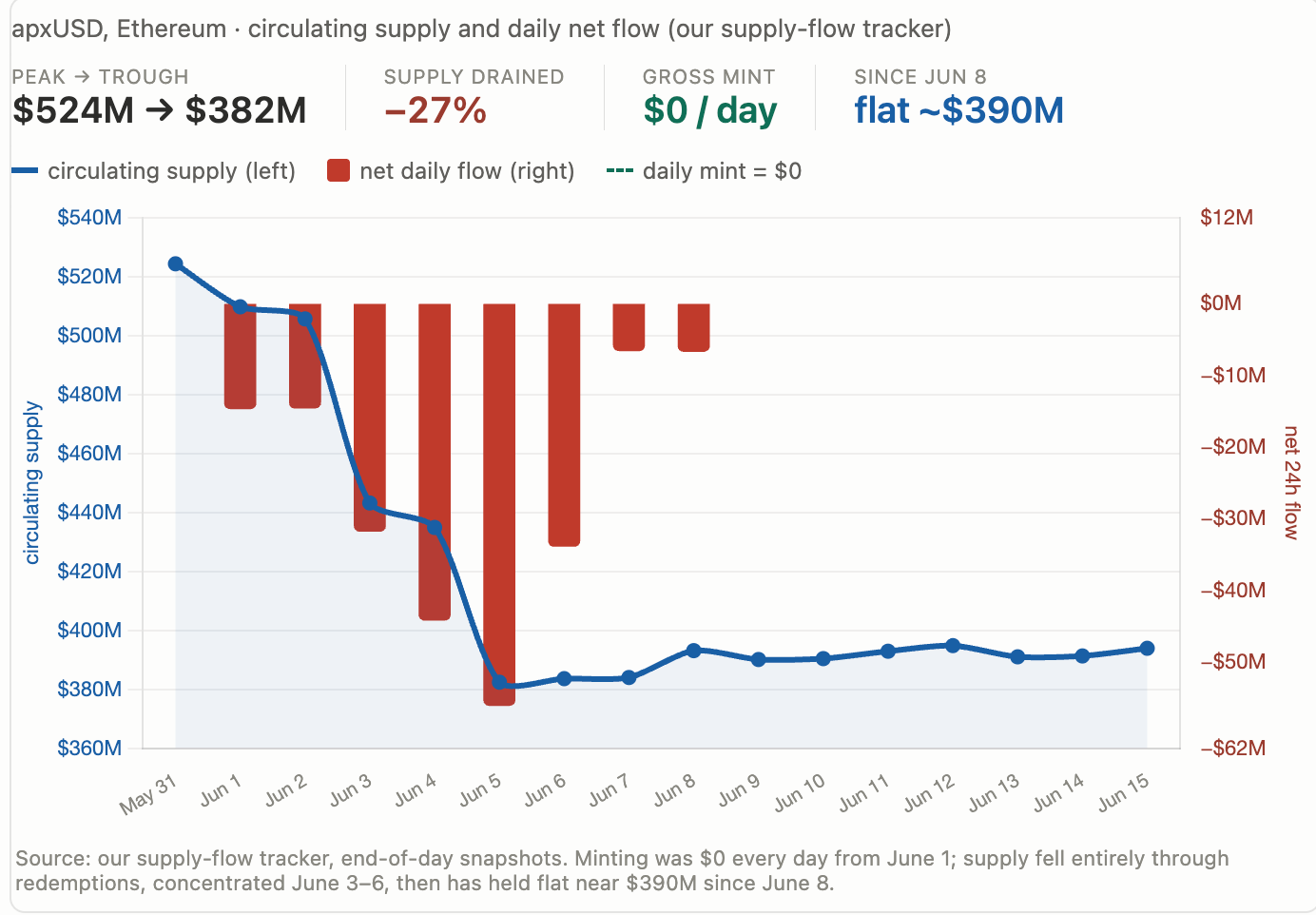

Our DD.xyz supply-flow tracker, which scores net mint and burn activity, picked up the redemption wave Apyx describes in its post-mortem: minting effectively stopped on June 1, and supply drained about $142M from its May 31 peak of $524M to a $382M trough, a 27% contraction concentrated over June 3–6, before holding flat near $390M from June 8 on.

Redemptions were the dominant flow, not new issuance, which is the signature of holders exiting into a discount rather than the protocol inflating supply. Solvent backing, real exit pressure, not minting.

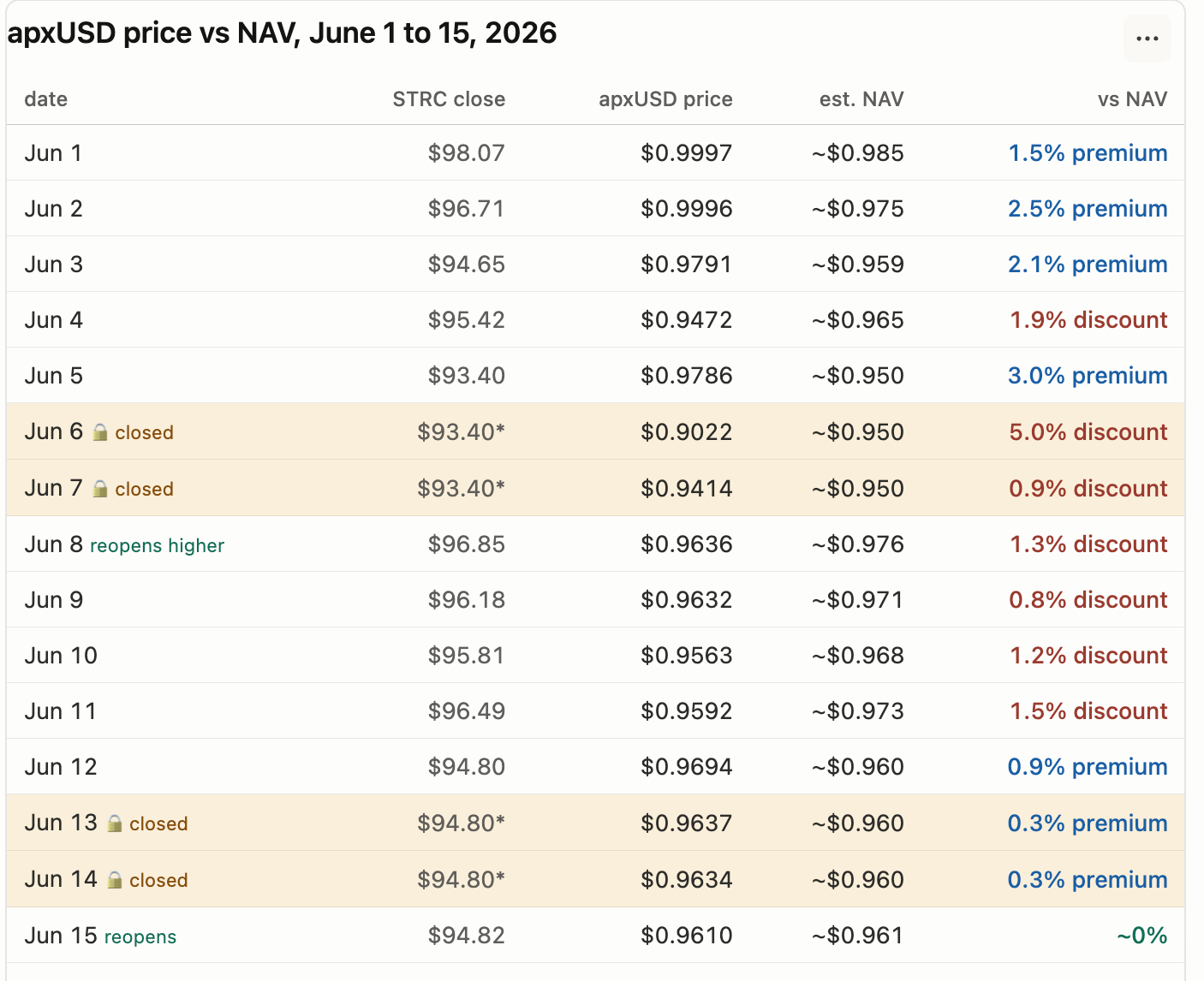

THE DISCOUNT, RECONSTRUCTED

STRC is a listed preferred share with a daily close, so we can rebuild the NAV. Model it as par

minus the STRC drawdown scaled by its weight in the basket, line that up against apxUSD's on-chain:

The table shows the full arc. Early on, apxUSD traded at a small premium to its NAV: the market held the peg while STRC had already dropped, so the price briefly sat ahead of its own collateral. Then it overshot the other way. The deepest discount, around 5% under NAV, hit on June 6, the closed-market weekend, when apxUSD was getting priced 24/7 off a stale Friday close. STRC reopened higher on Monday, $96.85 against the $93.40 close, and the discount closed over the following days. By mid-June apxUSD had converged back to its NAV.

Across a range of basket weights the trough discount sits between 4 and 6%, and that is the conservative version, since Apyx reports overcollateralization above 100%. Either way the point holds: at its worst apxUSD traded at a discount to a solvent NAV, not missing backing. It never returned to $1, and it did not need to. Its collateral is still about 5% below par, so apxUSD sits near $0.96, tracking its backing exactly as a NAV-follower should. This is the chart a structural-health view can draw and a price feed cannot: the peg broke because the collateral's market was closed, not because the collateral was gone.

MIMS Depeg Event

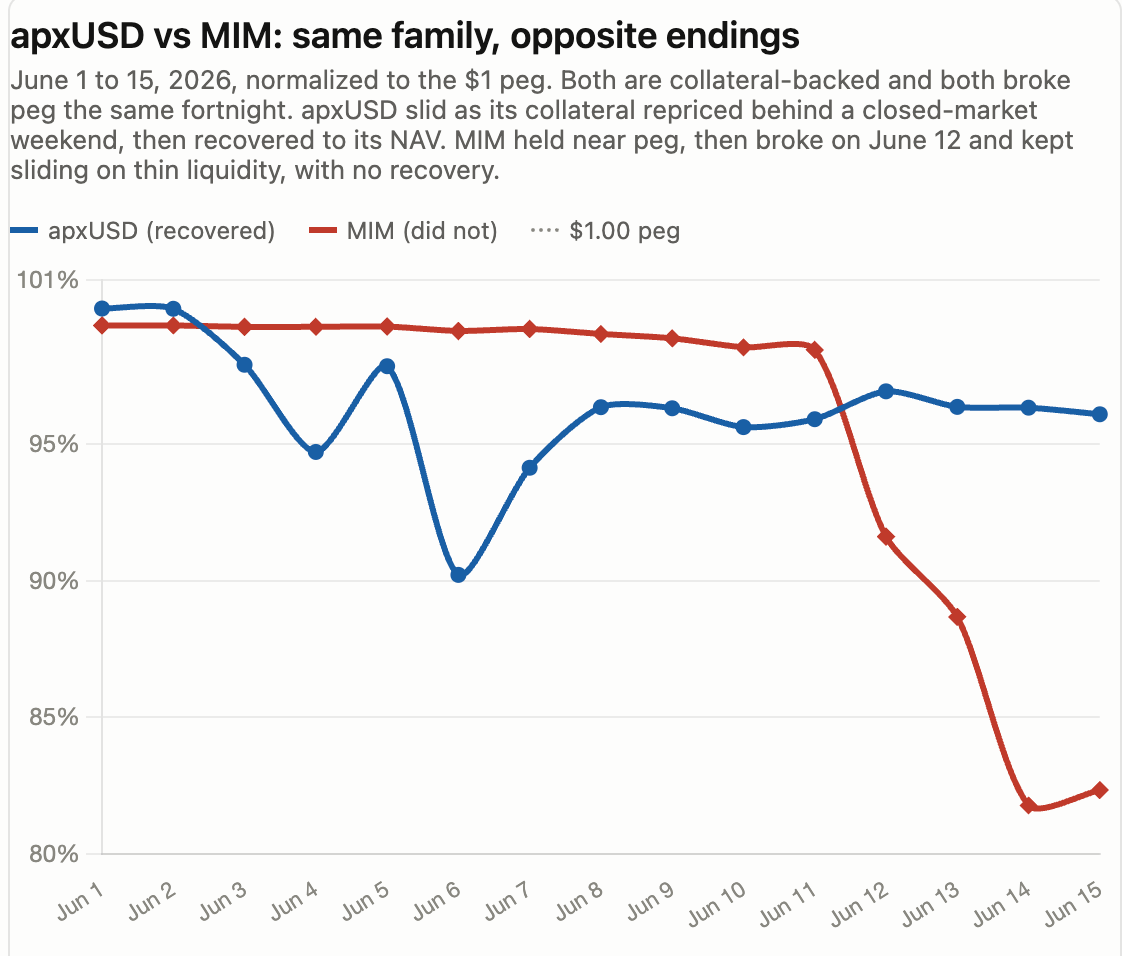

In the last couple weeks apxUSD discounted and recovered, MIM did something that looked similar on a price chart and meant something very different underneath. Magic Internet Money, the crypto-backed CDP stablecoin from Abracadabra, held near peg through June 11, broke on June 12, and unlike apxUSD has not recovered. It was not an exploit. The cause was liquidity. MIM has shrunk from billions at its peak to a roughly $24M token, with about $35M of fragmented on-chain liquidity spread across 47 pools on five chains and pool-balance health around 12%. When the broader Bitcoin route pushed sellers into those shallow pools, the price had nothing to support it.

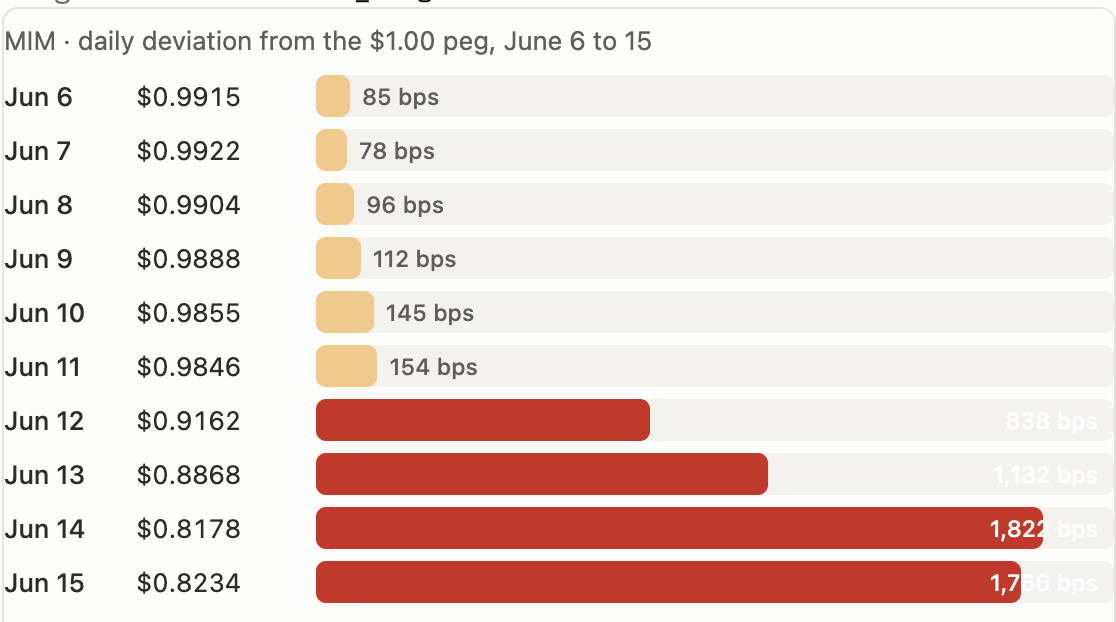

The daily deviation chart shows the shape of it. MIM drifted just under peg for a week, 78 to 154 basis points off, never quite at a dollar but never alarming. Then on June 12 it falls off a cliff: 838 bps, then 1,132, then 1,822 bps by June 14, roughly 18% below peg, where it has stayed. No gradual slide, no bounce. The token repriced down a step and held.

Put the two side by side and the contrast is the whole point. Both are collateral-backed and both broke peg the same fortnight. apxUSD dipped over a closed-market weekend and recovered to its NAV; MIM held, then broke and kept sliding. The difference was never solvency. It was whether the collateral could be sold deep enough, and fast enough, to bring the price back. apxUSD's could. MIM's is still recovering.

The pattern, and what it demands

These are only a sample. There have been plenty of depeggings this year, USR in March, StablR in May, apxUSD and MIM in the same week of June, and these are just the ones that show the categories most cleanly. Across even this handful we can see the contrast.. The earlier events were supply events, private key compromises and rogue mints where the backing actually gave way. The recent ones are increasingly collateral and market events, tokens that stayed solvent where the peg broke because the assets repriced or the liquidity to trade them was not there.

That matters because stablecoin depeggings look similar from the outside. apxUSD, MIM, and USR each printed a number under a dollar, and a naive price feed would have flagged all the same way. But one was a solvent token that recovered, one was a solvent token stuck behind dead liquidity, and one was an insolvent token that should never have minted what it did. The only thing that separates them is the structural read underneath the price: how the market price sits against NAV, whether reserves still cover supply, and whether there is enough liquidity to close a discount.

The mix is only going to tilt further, into preferred equity, tokenized treasuries, and Bitcoin-backed credit, each with TradFi hours, real collateral volatility, and thin on-chain liquidity. No two of these events looked alike, so we are training machine learning systems on the structural signatures of every depeg we study, supply velocity, NAV compression, collateral repricing, liquidity depth, cross-source divergence, to anticipate the next one and classify it correctly before the peg breaks. Each event sharpens the models, and the goal stays the same: read a depeg for what it really is, early enough to act on.

Closing

As stablecoins evolve from simple crypto-backed assets into financial instruments backed by preferred equity, tokenized treasuries, private credit, and other real-world assets, understanding risk requires far more than monitoring a price feed. The difference between a catastrophic insolvency event, a collateral repricing, and a liquidity-driven dislocation can determine whether a stablecoin recovers in hours, remains impaired for months, or fails entirely. Webacy continuously monitors these structural signals in real time, tracking collateral health, liquidity depth, redemption flows, supply velocity, NAV compression, cross-market divergence, and behavioral anomalies before they manifest as headline depegs. Our systems not only generate early warnings when risk conditions begin to emerge, but provide the intelligence layer needed to explain why an asset is moving and what is actually happening beneath the surface. As traditional finance increasingly converges with on-chain markets, bringing with it market-hour constraints, complex collateral structures, and interconnected sources of risk, real-time asset integrity monitoring becomes foundational infrastructure. The future of digital assets will not be secured by knowing that a peg broke. It will be secured by understanding the structural conditions that caused it, early enough to act before the market does.